Where Are The Shorts?

There is something unusual about our short ideas. Other hedge funds do not short our shorts. For the past eight quarters, only one of our short ideas showed up on the Goldman Sachs Hedge Fund VIP most-shorted list at quarter-end. This is remarkable. Given the number of short ideas and the length of the most-shorted list, there is almost no chance that this is happening by chance. Instead, hedge funds appear to be actively avoiding our short ideas. This is odd because most of the potential alpha in our investment approach is in our short ideas. Hedge funds need these short ideas, yet they won’t touch them. Any of them. How can this be?

We do source our investments from idiosyncratic, niche strategies. However, if we look across our short ideas - are there any characteristics that could explain the difference in our short approach? Yes. There is one glaring difference between our short ideas and that of the average hedge fund. We tend to short high-beta stocks and we tend to be long low-beta stocks. Meanwhile, popular hedge fund investments tend to do the opposite: they are long high-beta stocks and short low-beta stocks.

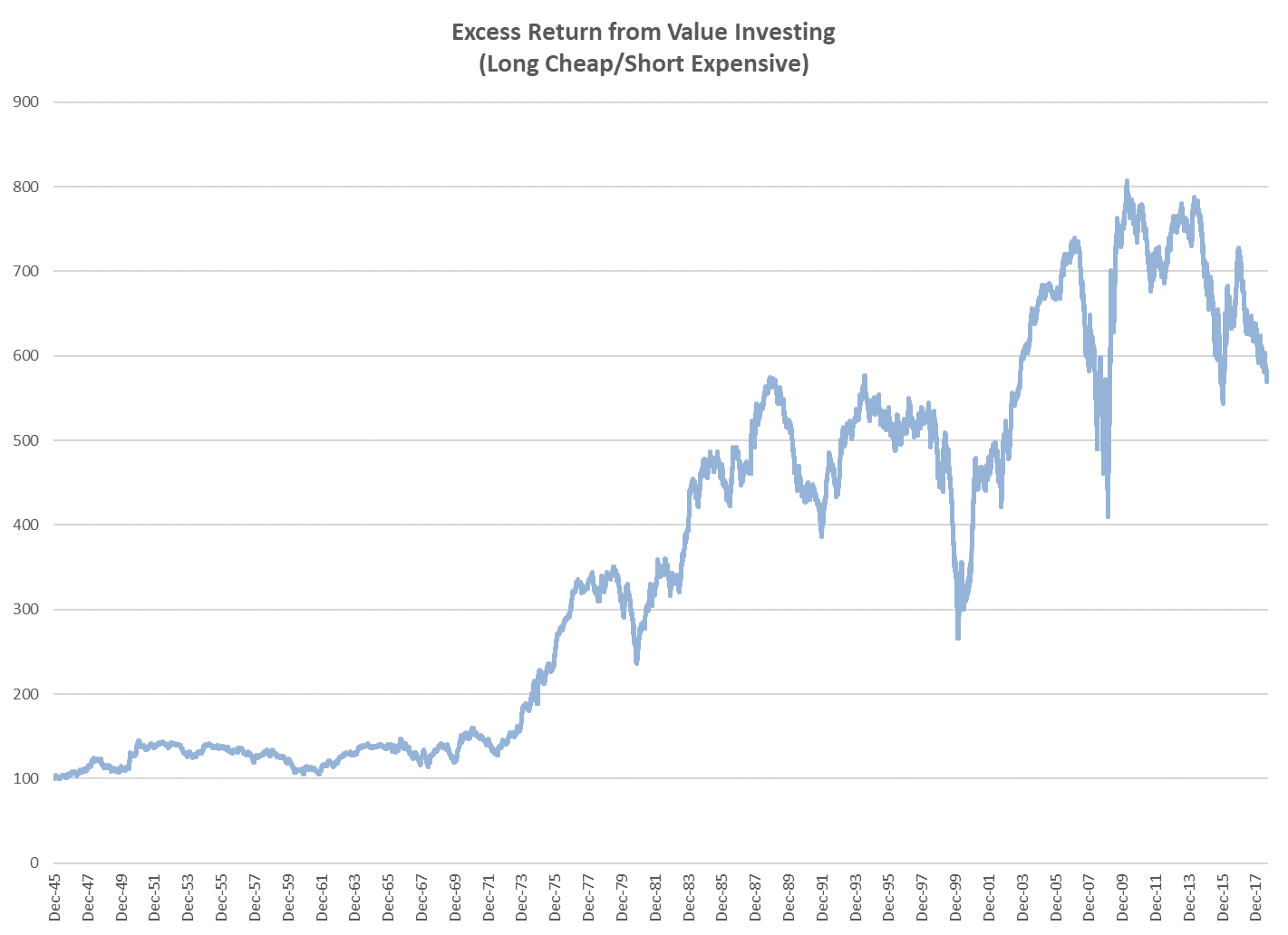

This difference in positioning has profound implications for performance in the long run. To understand how important this difference is, let’s start by looking at an investment strategy that is familiar and that we can all agree with – value investing. The returns from systematically going long cheap stocks and shorting expensive stocks in a market neutral manner are illustrated in the chart below. As you can see from the chart, being a value investor since World War II has been a good idea. Note that all of the data discussed herein is publicly available (here), uses standard, non-proprietary measurements, and covers the historical period back to World War II in the US.

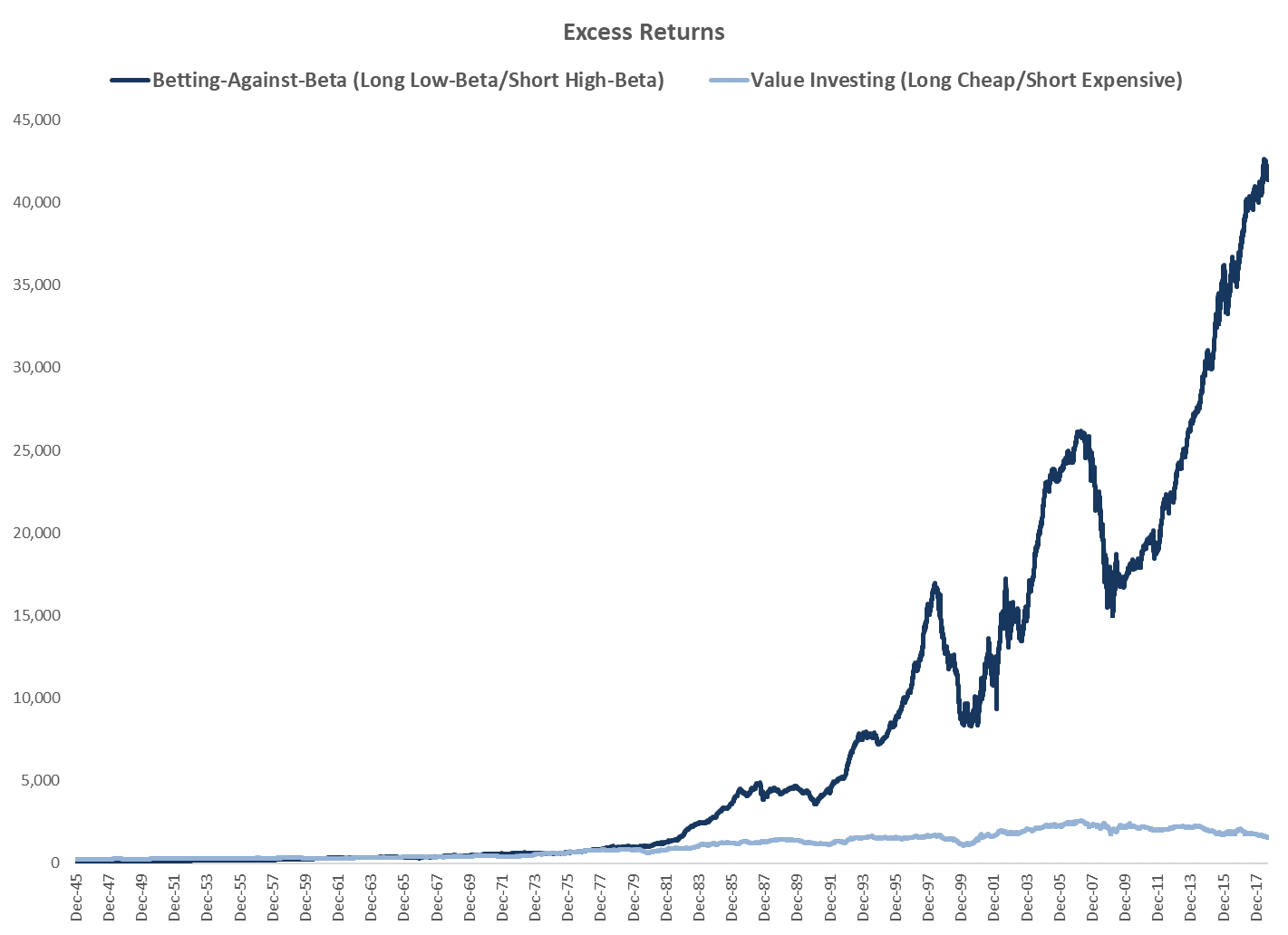

Now, let’s look at the returns from shorting high-beta stocks/going long low-beta stocks, which I will refer to as “betting-against-beta” from here on out. The idea of betting-against-beta is old and is not my invention. The excess returns from pursuing this approach systematically, in a market neutral manner, are in dark blue in the chart below. The chart also graphs the excess returns from value investing in light blue.

Betting-against-beta has more than 3x higher annual excess returns than being a value investor – 8.5% versus 2.4%. Plus the returns from betting-against-beta have similar volatility, but are more consistently positive, than value. Another feature of betting-against-beta that is of great interest – excess returns have stayed stable over the past century, while value investing returns have decayed as capital markets have institutionalized. That is not to say that value investing is bad – ideally you would both seek out value and to bet-against-beta. The point is more that if you believe value investing makes sense and is true, then the data suggests that betting-against-beta is potentially more true, more profitable, and deserves your undivided attention.

Naturally, at Bishop Rock, our overall portfolio is usually positioned like the dark blue line – we are short high-beta stocks/long low-beta stocks. I mean, to do otherwise, would be suicide for your portfolio. Yet, ours is a very contrarian approach. The average long/short equity hedge fund explicitly goes long high-beta stocks and shorts low-beta stocks, which is reflected in popular hedge fund ideas. Can you imagine trying to run a fund that - in addition to charging fees and paying commissions - has structured its portfolio so that it is running against such a strong alpha headwind? That would be crazy!

Nevertheless, this positioning is the norm among equity long/short hedge funds. Since hedge fund managers and allocators are smart, it is worthwhile understanding why they choose to lean into this strong alpha headwind and how it feeds the consistently high excess returns in the betting-against-beta strategy. The answer lies in the incentives hedge fund managers face.

To better understand manager incentives, in practice, I asked a large global prime broker to run the numbers for me on hedge fund flows – who receives inflows and who receives outflows. Approximately 85% of institutional hedge fund flows go to managers with top quartile, 3-year returns. These returns are the reported, nominal returns without risk adjustment. Meanwhile, the average hedge fund sees outflows. In addition, funds with top quartile 3-year track records and top quartile performance in the most recent year receive the bulk of the flows going to top managers. So as managers, those are our marching orders: produce top quartile headline returns, and they better be top quartile now, or your fund is dying.

Given these incentives, what would we expect a rational hedge fund manager to do? Well, it’s top quartile or bust. And allocators – in aggregate – do not penalize for risk-taking when markets are rising. The highest headline returns get rewarded with inflows. So managers respond to these incentives by loading up on high-beta stocks and going out the risk curve in order to have a chance at top quartile returns, and survival. This makes sense since markets rise 6 years out of 7 on average, so having a higher beta portfolio will, in theory, give a manager a better chance at delivering higher headline returns in most years. As a result, managers devote their clients’ capital to relatively high risk and high-return-potential ideas. And to add even more risk, managers tend to go short low risk, lower-return-potential stocks. This bad behavior is not limited to hedge fund managers: mutual funds structurally overweight high-beta stocks and underweight low-beta stocks, and this dynamic gets worse the greater the institutional ownership of a mutual fund. In short, managers buy lottery tickets with their clients’ capital and, on average, lottery ticket winners get rewarded with more capital.

The net result of this behavior across the capital markets is that high risk stocks (i.e. lottery tickets) are structurally overvalued and low risk stocks are undervalued over time. This dynamic causes the counterintuitive phenomenon that high-beta stocks underperform low-beta stocks, risk-adjusted, in the long-run. By a lot. The chase for performance and the disregard for risk management are not unique to the United States. The persistent desperation of managers to produce performance and the effectiveness of betting-against-beta are found across liquid markets and across time. Betting-against-beta is an efficient way to profit from the entrenched agency costs in institutional investment management. Indeed, the returns available from betting-against-beta are higher and more consistent than those available from other factors such as value, momentum, and size. As a practitioner of investing, I can't say that I am surprised.

At Bishop Rock, our investment strategy is not explicitly focused on betting-against-beta. We develop niche, predictive strategies to source ideas, use fundamental analysis to select the best ideas from these strategies, and arrange the best ideas into a portfolio that meets our goals. We are, however, careful to ensure that the information that we use to make decisions, and the strategies we use, are predictive of positive future returns. As a result, our approach tends to overlap with characteristics that are predictive, like betting-against-beta. We have found that conventional investment wisdom is often different from what is predictive. What we do is monetize those differences. Betting-against-beta is one simple example of this phenomenon that is easy to explain.

As we look forward to 2019, the key to better performance is not more stock picking. It is not big data. Or boiling the ocean with more research. The key to better performance is to stop allocating capital explicitly or implicitly to investment strategies that have little hope of producing excess returns in the long run. You can’t stock pick your way out of a failed strategy in the long-term. And you don’t want to pay fees to watch someone try. In 2019, do the work, run the numbers yourself, and make sure you are spending your time picking stocks within predictive, cross validated investment strategies.

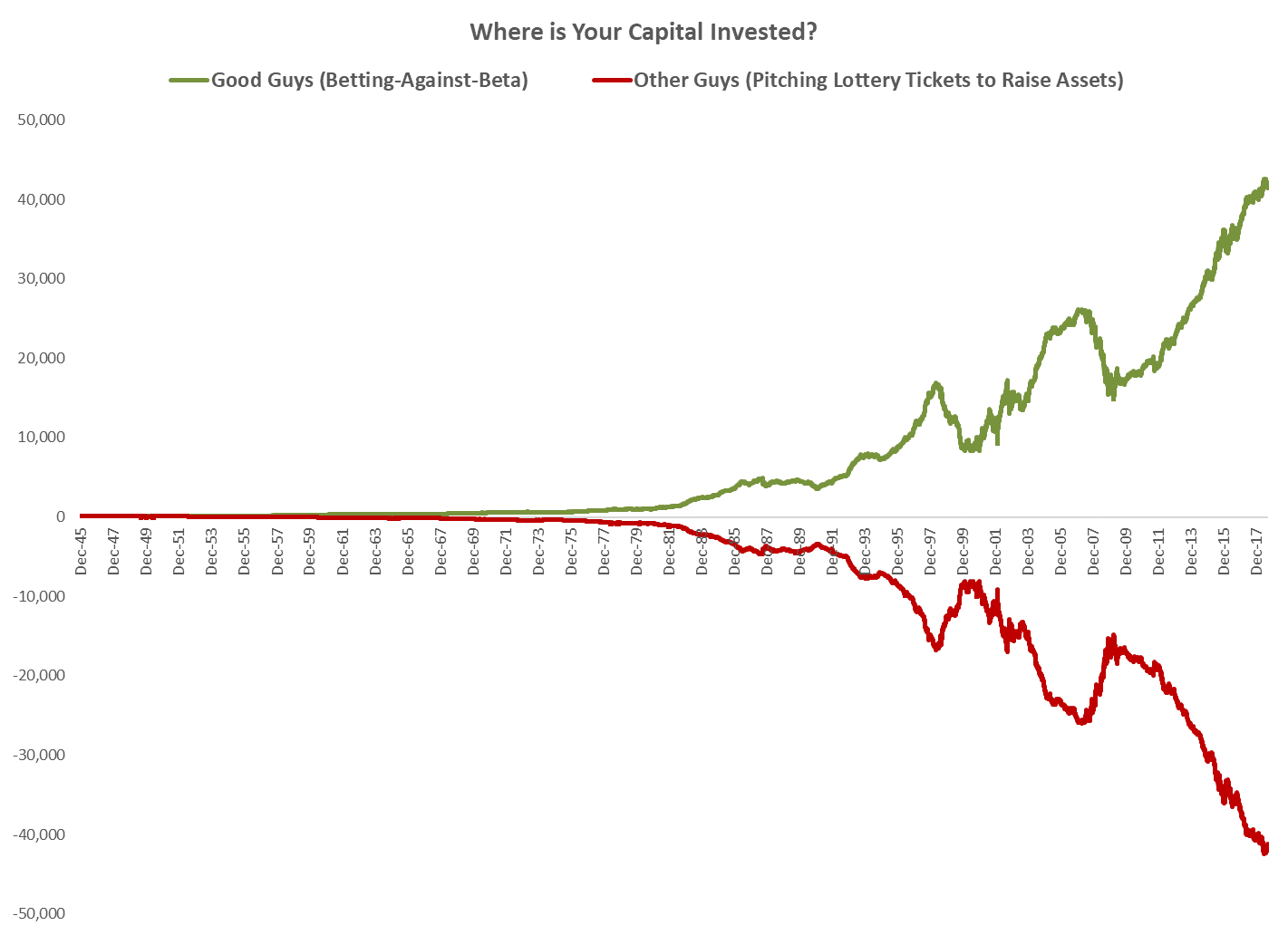

To leave you with an image, I have charted the returns from betting-against-beta (green line) and from doing the opposite below (red line). I love doing stock research and want a bottoms-up best ideas portfolio. But for goodness sake, get your investment process, and capital off of the red line and onto the green line. If you don’t, the markets will do it for you by reallocating profits from the Other Guys to the Good Guys in the long run.

DISCLAIMER:

THIS ARTICLE REPRESENTS THE VIEWS OF BISHOP ROCK AS OF THE DATE OF PUBLICATION AND THE INFORMATION CONTAINED HEREIN IS SUBJECT TO CHANGE WITHOUT NOTICE AT ANY TIME. ALL INFORMATION PROVIDED IS FOR THE RECIPIENT ONLY AND SHALL NOT BE COPIED OR TRANSMITTED TO ANY OTHER PERSON. WHILE THE INFORMATION PRESENTED HEREIN IS BELIEVED TO BE RELIABLE, NO REPRESENTATION OR WARRANTY IS MADE CONCERNING THE ACCURACY OF ANY DATA PRESENTED. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

THIS ARTICLE SHALL NOT BE CONSIDERED AN OFFER TO BUY OR SELL A PARTICULAR SECURITY OR AN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY INTERESTS IN ANY FUND MANAGED BY BISHOP ROCK OR ANY OF ITS AFFILIATES. SUCH AN OFFER TO SELL OR SOLICITATION OF AN OFFER TO BUY INTERESTS MAY ONLY BE MADE PURSUANT TO DEFINITIVE SUBSCRIPTION DOCUMENTS BETWEEN A FUND AND AN INVESTOR.